") BAWANA IN NORTHWEST DELHI is a telling stop on India’s winding and elusive gas trail. About 35 km from the city centre, Bawana is where the Delhi government is setting up a 1,500 MW power plant that will meet a fifth of the capital’s voracious energy needs. The state-owned generating company, Pragati Power Corporation Ltd (PPCL), is forking out Rs 4,500-crore to set up this gas-fired plant in two modules of 750 MW each, the first of which has been ready for a while. However, despite severe power cuts in recent weeks, the plant has remained idle. There is no fuel to run it

BAWANA IN NORTHWEST DELHI is a telling stop on India’s winding and elusive gas trail. About 35 km from the city centre, Bawana is where the Delhi government is setting up a 1,500 MW power plant that will meet a fifth of the capital’s voracious energy needs. The state-owned generating company, Pragati Power Corporation Ltd (PPCL), is forking out Rs 4,500-crore to set up this gas-fired plant in two modules of 750 MW each, the first of which has been ready for a while. However, despite severe power cuts in recent weeks, the plant has remained idle. There is no fuel to run it

The PPCL project, whose second gas turbine was synchronised on February 9 this year, is one of 14 power projects that desperately needs fuel supplies to go on line. A total of 8,200 MW of gas-based generation capacity will near completion by March 2012, according to the Central Electricity Authority (CEA), which keeps tabs on projects countrywide. Although the private sector is the dominant promoter of the gas-based projects, which will add much-needed megawatts to the Eleventh Plan power target, developers caught in the fuel trap include public sector undertakings and state governments.

The Bawana project has been luckier than most, primarily because it feeds Delhi. Letters have been flowing thick and fast between the Sheila Dikshit government and the Ministry of Petroleum and Natural Gas (MoPNG), not to mention the Prime Minister’s Office, about the precarious future of the project if it is denied gas from Reliance Industries Limited’s (RIL’s) D6 field in the offshore Krishna-Godavari (KG) Basin at the government-approved rate of US $4.20 per mmBtu (million British thermal units). Parimal Rai, principal secretary, power, Government of the National Capital Territory of Delhi, says the economics of the project would go for a toss unless it gets the promised gas from Oil and Natural Gas Corporation (ONGC) and KG D6 (see ‘Precarious economics of Bawana power project’). “We cannot sell power at a reasonable rate unless we get KG D6 gas,” frets Rai, who is chairperson of PPCL.

The project needs 2.7 million standard cubic metres daily (mmscmd) for the first module, about 0.93 mmscmd having been promised from D6. He has put work on the 750 MW Bamnauli project, for which land has been acquired, on hold till the fog over gas supplies clears.

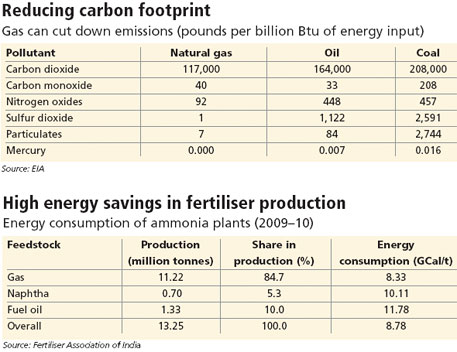

There are fertiliser projects, too, that would be left high and dry. According to the Fertiliser Association of India (FAI), producers have invested Rs 5,000 crore for ramping up capacities and for switching from the criminally expensive fuel oil and naphtha feedstock to gas. An FAI official says as the world’s second largest consumer of fertiliser, it is vitally important for India to have assured supplies of gas for this industry, which has seen no greenfield investments in the past 15 years.

Victims of the gas shortage are many. There is, for instance, city gas distributor Bhagyanagar Gas Ltd (BGL) of Andhra Pradesh which has been waiting for six months for the tap to be turned. Says C A Rashid, managing director, BGL: “We have been on the verge of getting gas supplies since April this year. RIL could not supply us the promised 0.1 mmscmd from its KG D6.” Its hopes were renewed in September. That was when the BGL official had visited petroleum and natural gas minister S Jaipal Reddy and had personally taken a letter confirming supplies through a swap deal worked out between GAIL India and RIL. BGL, a joint venture between public sector Navratnas, GAIL (India) and Hindustan Petroleum Corporation, has been sitting on idle assets of Rs 150 crore since April apart from incurring a loss of about Rs 90 lakh daily because its main Shamirpet gas station in Hyderabad could not be commissioned, the company claims.

Victims of the gas shortage are many. There is, for instance, city gas distributor Bhagyanagar Gas Ltd (BGL) of Andhra Pradesh which has been waiting for six months for the tap to be turned. Says C A Rashid, managing director, BGL: “We have been on the verge of getting gas supplies since April this year. RIL could not supply us the promised 0.1 mmscmd from its KG D6.” Its hopes were renewed in September. That was when the BGL official had visited petroleum and natural gas minister S Jaipal Reddy and had personally taken a letter confirming supplies through a swap deal worked out between GAIL India and RIL. BGL, a joint venture between public sector Navratnas, GAIL (India) and Hindustan Petroleum Corporation, has been sitting on idle assets of Rs 150 crore since April apart from incurring a loss of about Rs 90 lakh daily because its main Shamirpet gas station in Hyderabad could not be commissioned, the company claims.

This has had a spiralling effect. City gas distribution typically includes, in addition to piped natural gas to residences, commercial complexes and industries, CNG for public transport (buses, taxis and autorickshaws). But the sector is not viable unless adequate domestic gas is made available to it (see ‘City gas takes a knock’). In Hyderabad, the Andhra Pradesh Road Transport Corporation has been suffering another set of losses with around 250 buses in its fleet converted to run on CNG but stuck for want of fuel.

")

While coal is the most villainous of fossil fuels, natural gas is the cleanest. It emits 30 per cent less carbon dioxide than oil and 45 per cent less carbon dioxide than coal (see ‘Reducing carbon footprint’). In the case of power generation, gas-fired combined cycle units can be up to 60 per cent energy efficient, whereas coal and oil generation units are typically 30-35 per cent efficient. This is not the only reason there is a mad scramble for this fuel in gas-starved India. It is also cheaper and more efficient to use, especially in the fertiliser industry. The government has played a crucial role in allocating its supply to the core and non- core sectors in a changing order of priority, although historically the fertiliser industry and the power sector have been given the bulk of the supplies. In addition to the 2008 gas utilisation policy, which took away the right of producers to sell gas to customers of their choice, the Empowered Group of Ministers has periodically been changing the list of who should get the first shot at gas after fertiliser and power. Accordingly, city gas distribution, LPG extraction and sectors such as steel, petrochemicals and refineries figured on the list only after the demands of the core sector were met.

The current situation, in which natural gas has become synonymous with a snowballing crisis, is a complete swing from the euphoria of plenty in 2009-2010, when the D6 field was gushing, pumping in increasingly larger amounts of gas into the economy. From 10 mmscmd in April 2009 supplies had shot up to over 40 mmscmd by June, making it appear that the optimistic forecasts of 2002, when RIL discovered the biggest natural gas reserves in the country, were indeed on track. The company had said then that gas supplies would thereafter touch 80 mmscmd.

But hopes of India switching largely to a cleaner fossil fuel have dipped dramatically in the past year as RIL, first caught in bitter legal disputes over pricing and contracts, has tapered off its production from 60 mmscmd to 46 mmscmd. Till 2009, most of the gas was produced by the state-owned behemoth, ONGC. But in 2009-10, when the total production touched 46.5 billion cubic metres (bcm), it accounted for only 23.1 bcm, while RIL produced as much as 14.4 bcm. Apart from the scabrous court case between the Ambani brothers that pitted RIL against Reliance Natural Resources Ltd for four years starting in 2006 and also involved the public sector undertaking NTPC, the country’s largest power generator, there have been other controversies. The most serious was kicked off when the Comptroller and Auditor General of India (CAG) raised questions about RIL’s high capital expenditure in D6 and what it termed the capitulation of the downstream regulator, the Director General of Hydrocarbons (DGH), to the company’s terms. All of this has done little to bring any clarity to the situation.

So far, RIL has refused to say when production will be ramped up. Although it has hinted at technical glitches—drop in reservoir pressure and water ingress—DGH has blamed it for not drilling an adequate number of wells. RIL has not responded to Down To Earth’s questions either. However, its partner BP, which has picked a 30 per cent stake in 23 of its oil and gas fields for US $7.2 billion, has stated publicly that it will take till 2014 to jack up production. At the September 28 press briefing, BP chief Robert Dudley described D6 as “a world class resource” but also said it was a “complex reservoir” that called for high technology. “You are trying to imagine down miles under the sea, (but) it is not quite as you expect. You find some surprises. So the field has declined and our teams and Reliance teams are working on that,” he said.

The popular theory doing the rounds is that RIL is not keen to jack up production till 2014 when the price of gas from KG D6 comes up for review. In a price discovery exercise it conducted in 2007, the company had wanted its D6 gas fixed at $4.5 per mmBtu and the government had approved it with a slight modification—to $4.205 per mmBtu—during the first five years of production. Dudley’s statement and indications from RIL have tended to reinforce this perception.

Whatever the reasons for the shortfall, no one is optimistic about the prospects of gas in the short term. Bleak is the refrain to be heard both in MoPNG and in the Ministry of Power. “Where is the gas,” asks an official from MoPNG, responding to frequent petitions sent out by the Delhi-based Association of Power Producers on projects left in the lurch. Ironically, the uncertainty comes at a time when the Indian market is being viewed as one of the fastest growing in the world. The International Energy Agency (IEA), an autonomous institution, says the potential for growth is tremendous but pricing would be a key factor in pushing up consumption figures. India is an extremely price-sensitive market because the ability of customers to pay varies widely. Fertiliser producers are subsidised by the government—the current year’s subsidy is estimated at Rs 70,000 crore—and have very little leeway in absorbing higher prices. The power producers have to keep in mind what the market can bear since gas has to compete with coal for base load generation.

Rai of Pragati Power explains the huge difference in the cost of power based on different sources of gas: “The Bawana project becomes unviable if, instead of the government-approved rate of $4.2 per mmBtu, it has to buy spot LNG at $12-16 and regassify it. In this case, the unit cost of power almost doubles to Rs 8. There will be no takers.” There has to be a paradigm shift in the government’s approach to utilising gas for the power sector, says Ashok Khurana, director general of the Association of Power Producers. “If the government sees gas as benign fuel that reduces the carbon footprint it needs to sit down and decide on pooling of prices. More important, it also needs to free up the market for power generators as laid down in the Electricity Act.” His contention is that gas-fired thermal plants offer a range of benefits apart from the environmental incentives to power-starved India: faster response time to varying load, cheaper to set up because projects come up faster and a diversification of the energy security risks.

| |

Popular belief is that RIL is not keen to jack up production till 2014 when the price of gas from its D6 field will be due for review |

|

| |

|

|

But one of the key demands of the association, pooling of gas prices, has already been rejected by a government-appointed panel to look into the issue. The panel, headed by Planning Commission member Saumitra Chaudhari, said in a report submitted end-August that domestic natural gas users should not be forced to subsidise costlier liquefied natural gas (LNG). It did not recommend a pooling mechanism at the overall level or on a sectoral basis.

It said preferential allotment of domestic gas should only be for priority sectors, such as fertilisers and power, and other consumers such as steel plants be allocated imported LNG. While domestic gas is currently priced between $4.2 and $5.5 per mmBtu, LNG, imported in ships, costs $12 to $16 per mmBtu. “The non-priority users operate in a market environment where their output prices are market-driven with no regulatory burden and hence they should be able to pass on the higher costs of gas feedstock,” it said.

What then is the outlook for gas consumers in the country? Cheaper gas that could have been brought by cross-border pipelines is proving to be a mirage (see ‘

The pipeline mirage’) and even long-term LNG contracts will now be steeply higher than the current $3.12-5.5 mmBtu. The country currently imports around 7.5 million tonnes annually under long-term agreements signed with Qatar.

What is clear is that although latent demand does exist from the unregulated sectors, consumption will depend on gas being available at reasonable price. According to an analysis by Edelweiss Securities, gas consumption between 2011 and 2014 will be suppressed and grow at compound annual rate of four per cent against the expected GDP growth of seven-eight per cent. Unsurprisingly, consumption by the fertiliser and power sectors will be largely limited to indigenous supply, while most of the incremental LNG supply will be taken up by city gas distributors and industrial consumers.

The gas bubble, it appears, will last for quite a while.

")

Iran President M Ahmadinejad, Hillary Clinton and Turkmenistan head G Berdimuhamedov")